{kind=link}

Sue Cho and Kyle Davis’ latest bankruptcy drama

OX.FUN, a memecoin exchange platform Emerged from the remains of the Open Exchange (OPNX)found itself at the center of insolvency rumors this week after freezing user deposits amounting to $1 million.

The controversy erupted on February 21, when X user JefeDAO on X claimed that one of its members had deposited $1 million in USDC at OX.FUN, only to find the funds locked moments later. According to JefeDAO, the platform accused the user of violating its terms of service.

Nicholas Pyle, founder of OX.FUN, responded to the allegations, stating that the user did just that I tried to exploit The platform. OX.FUN He claimed The individual engaged in “market manipulation” to gain $120,000 in OX tokens, which resulted in the freeze. Exchange He added An agreement has been reached with JefeDAO, the account has been restored and the original deposit will be refunded.

The incident sparked scrutiny of OX.FUN’s financial standing, with Coinbase CEO Conor Grogan noting that most of the exchange’s holdings appeared to be in its tokens, a potential red flag for liquidity concerns. The situation worsened as OX tokens lost significant value amid the controversy, sparking speculation about the platform’s solvency.

OX.FUN dismissed these concerns, It is useful Tracked portfolios do not reflect the full extent of the platform’s reserves. An OX.FUN team member told the magazine in a Telegram message that all user funds are backed 1:1 and said the exchange will launch a transparency dashboard “in the coming days.”

Adding to the scrutiny is OX.FUN’s ties to Kyle Davies and Sue Zhou, co-founders of collapsed Singapore-based hedge fund Three Arrows Capital. The company, once one of the largest in crypto, collapsed in 2022 after making aggressive leveraged bets that collapsed during a market downturn, leaving creditors billions of dollars in debt. After its collapse, Davies and Chu launched OPNX, a trading platform for bankruptcy claims, which was later shut down and replaced by OX.FUN, where Davies and Chu officially serve as advisors.

Bybit declares war on North Korean pirates

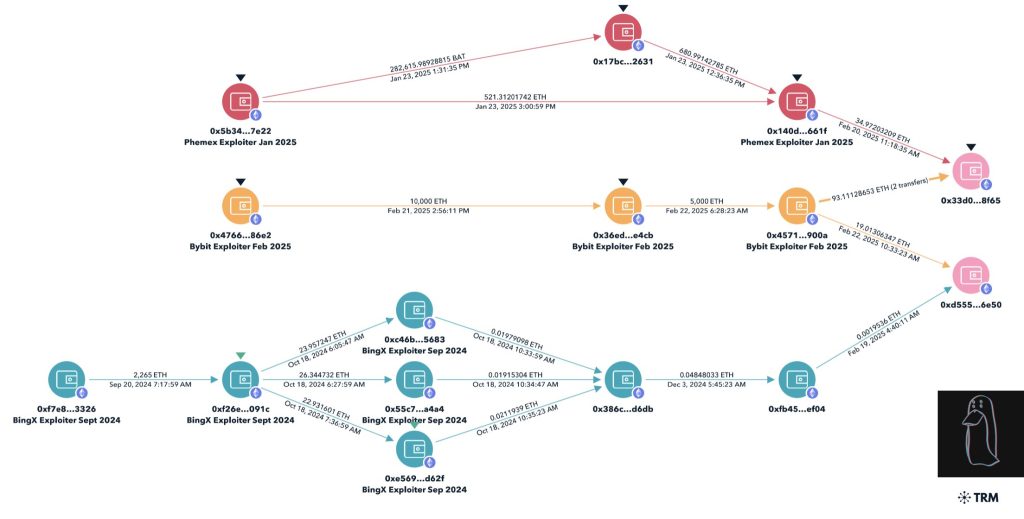

Bybit suffered the largest exploit in history on February 21, losing more than $1.4 billion to North Korean hackers.

Crypto investigator ZachXBT was the first to officially and publicly identify the hackers, receiving a bounty set by Arkham for providing definitive proof of their identity. He did this by linking a popular address used in the Bybit exploit to previous hacks against Asia-based exchanges BingX and Phemex, both of which were also attributed to the Lazarus Group. FBI later He confirmed that the attack was carried out by Lazarus.

Bybit lost 401,000 Ether in this exploit, and the hackers quickly distributed the funds across multiple wallets, eventually leading to over 11,000 wallets being identified. According to investigators at Elliptic.

One feature of the North Korean hackers, apart from dividing the funds into different wallets, is to convert them into local assets such as Ether before exchanging them for Bitcoin. Crosschain swap platform THORChain, which allows direct swapping of assets such as Ether to Bitcoin, has seen a huge increase in swap volume, It exceeded one billion dollars in less than 48 hours From February 26th.

After losing money to North Korea, PayBit War was declared against the E-Unit in the isolated kingdom It received industry-wide support from partners and competitors in tracking and freezing the funds.

However, eXch, a KYC swap platform, He refused to freeze illicit funds Linked to the Bybit exploit. EXch denies money laundering for North Korea.

Read also

Features

2026 is the year of practical privacy in cryptocurrencies: Canton, Zcash and more

Features

E for Estonia: How Digital Natives Are Creating the Blueprint for a Blockchain Nation

South Korea’s largest exchange has been banned from accepting new users

South Korean regulators have dealt a devastating blow to the country’s largest cryptocurrency exchange, Upbit, imposing a three-month business suspension and sacking of executives.

On February 25, FIU Announce Disciplinary action against Upbit and its executives for violating the rules of the game Reporting and Use of Certain Financial Transaction Information Act.

The sanctions effectively freeze Upbit’s ability to process new customers’ cryptocurrency deposits and withdrawals for three months. Nine executives were disciplined, including CEO Lee Seok-woo, who received a formal warning, and the company’s compliance officer, who was immediately fired — the first time a compliance officer at a South Korean cryptocurrency exchange has been fired by regulators.

Authorities accused Upbit of violating repeated warnings by participating in nearly 45,000 transactions with unregistered offshore exchanges. Regulators also found failures in customer verification, which allowed unsupervised trades despite strict financial compliance requirements.

Despite overseeing these violations, Seok-woo received nothing more than a slap on the wrist, with regulators citing his role as a supervisor rather than a direct participant in the misconduct.

While the sanctions are among the harshest ever imposed against a South Korean cryptocurrency company, Upbit downplayed their significance, insisting that trading services, fiat deposits and cryptocurrency exchanges will not be affected.

Speaking to local reporters, Upbit He said The stock exchange is examining all options, including legal avenues, to challenge the sanctions.

Read also

Features

2026 is the year of practical privacy in cryptocurrencies: Canton, Zcash and more

Features

E for Estonia: How Digital Natives Are Creating the Blueprint for a Blockchain Nation

Vietnam rejects sandbox proposal for cryptocurrency payments

Vietnam’s Ministry of Finance (MoF) has rejected a proposal to introduce cryptocurrency transactions in the country’s upcoming financial centers, citing concerns about financial security and regulatory gaps, state media Hanoi Times reported. I mentioned.

The decision is a setback for efforts to position Ho Chi Minh Cities and Danang as fintech hubs, as the government remains wary about the risks associated with cryptocurrencies and digital assets, which remain unregulated in Vietnam.

Vietnam’s Ministry of Planning and Investment has proposed launching a regulatory sandbox that would allow digital transactions in the country’s new financial centers, scheduled to start on July 1, 2026.

However, the Ministry of Finance opposed the timeline, noting that without a legal framework governing digital assets, such transactions pose significant risks. Officials reportedly stressed the need to put in place laws covering issuance, trading, service licensing and cybersecurity before digital assets are allowed into Vietnam’s financial system.

The ministry urged other regulatory bodies, including the State Bank of Vietnam, to express their opinion on the matter, as the potential use of digital currencies for payments falls within the jurisdiction of the central bank.

The Ministry of Finance also recommended that the government take direct control of any pilot program and remove the start date of July 1, 2026 from the proposal.

Subscribe

The most engaging reads on blockchain. It is delivered once a week.

Johan Yuen

Johan (Hysop) Yuen is a Cointelegraph staff writer and multimedia journalist who has been covering blockchain-related topics since 2017. His background includes roles as an assignment editor and producer at Forecast, as well as technology and policy-focused reporting positions at Forbes and Bloomberg BNA. He has a degree in journalism and owns Bitcoin, Ethereum, and Solana in amounts that exceed Cointelegraph’s disclosure threshold of $1,000.